.jpg)

The strongest jobs week we’ve seen in a long time was followed by surprisingly robust existing home sales and a relatively mild rise in “core” CPI. The Fed will meet next week, with no change to policy interest rates expected.

BLS jobs report capped off a very strong jobs week. The US economy added 172K jobs in May (vs. 85K expected), and the previously reported figures for March and April were revised UPWARD by 93K jobs. The unemployment rate was steady at 4.3%, and annual wage growth was running at +3.6% year-over-year.

TP: This was a strong report. We’re used to seeing downward revisions to prior months, big contributions from the birth-death model, and labor force reductions that keep the unemployment rate high. Not this time, though. The only underlying concern was the continued ‘replacement’ of full-time jobs with part-time ones.

Existing home sales rose, despite higher rates. May existing home sales climbed 3.2% month-over-month (also +3.2% YoY) to 4.17 million units (SAAR). That’s the highest figure we’ve seen since December 2025, which is quite impressive considering that 30-yr mortgage rates were hovering around 6.50% in May 2026. Median sales prices rose 1.3% YoY to $429K.

TP: Have we finally broken free from the 4 million unit sales pace we’ve been stuck at for more than 3 years? I’m watching two regions closely. First, is the South (~47% of total existing home sales), where transaction volumes appear to be rebounding thanks to improved affordability. The second, is the West (18% of total existing home sales), where key markets like San Francisco are on a tear.

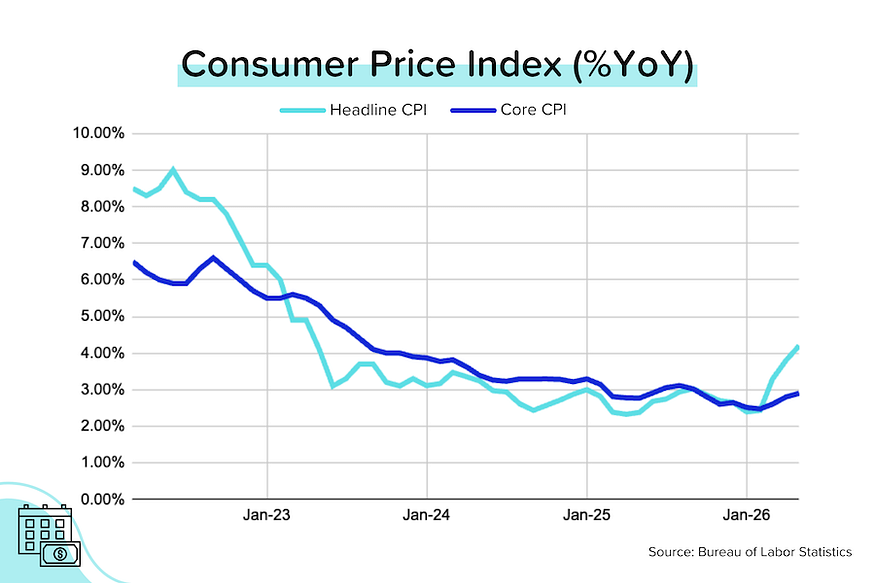

“Core” CPI barely budged. The bad news was that “headline” CPI jumped to +4.2% YoY in May (from +3.8% YoY in April). Driving the increase was a 41% YoY rise in the price of gasoline because of, well you know. The much better news was that “core” CPI (which excludes food & fuel prices) only rose to +2.9% YoY in May (from +2.8% YoY in April).

TP: Almost ALL of the monthly growth in “core” CPI came from two items: Shelter costs (which rose 0.3% MoM and have a 44% weighting in “core” CPI), and Airline fares (which rose 2.7% MoM and have a 1.7% weighting in “core” CPI). Almost everything else in “core” was flat to down MoM (e.g., used car prices and motor vehicle insurance premiums declined). And obviously, airline fares are affected by higher jet fuel prices.

How Much Has Affordability Improved?

Flattish prices at the national level obscure some large price drops at the metro level. Let’s use Austin and Miami as examples. Since mid-2022, median listing prices in Austin-Round Rock have dropped from $629,479 to $475,000. That’s a total drop of 24.5%! Over the same time period, prices in Miami-Fort Lauderdale fell 20.2%.

As the Fed began aggressively raising rates, average 30-yr mortgage rates hit a peak of just over 8% in October 2023. By that time, Austin prices had already dropped to $549,900 (-12.6% from the peak) and Miami prices had eased to $598,500 (-4.2% from the peak).

If you combine the two (lower prices and lower rates) between October 2023 and today, your monthly mortgage payment (principal and interest only) would be $800-$1000/month cheaper today. I’m not saying it’s cheap, just cheaper.

Bond and Mortgage Market

The Federal Open Markets Committee will meet next week (June 19) to discuss and vote on its interest rate policy. This will be the first meeting for the new Fed Chair (and Trump appointee), Kevin Warsh. With inflation rising and the job market strengthening, a rate cut is extremely unlikely. At the same time, a rate hike doesn’t seem justified either. Most of the rise in inflation is coming from energy prices (US/Iran conflict).

Note: The Fed Funds Rate policy range is currently 3.50–3.75%. The probabilities below come from the CME Group website and are implied from the Fed Funds Rate futures market.

- June 17 FOMC Meeting: This will be Kevin Warsh’s first meeting as the new Fed Chairman. 98% probability that the Fed Funds Rate will be kept at 3.50–3.75% (was 96% last week).

- July 29 FOMC Meeting: 88% probability that the Fed Funds Rate will be kept at 3.50–3.75% (same as last week) 11% probability that rates will be 25 basis points HIGHER than they are today.

- September 16 FOMC Meeting. 62% probability that the Fed Funds Rate will be kept at 3.50–3.75% (was 72% last week). A 34% probability that rates will be 25 basis points HIGHER than they are today (was 23% last week).

- Rate hikes in late 2026? If I look way out to the last FOMC meeting of the year (Dec 9), the market is pricing in a 32% probability (was 46% last week) that the Fed Funds Rate will be exactly where it is today. But the market is also pricing in a 67% probability that rates will be at least 25 basis points (and maybe 50 basis points) HIGHER by year-end!

They Said It

“More Americans are on the move, with home sales rising to the highest level since December. This is great news for the housing market and the economy. Improving affordability is helping drive this momentum. Even with mortgage rates ticking up compared to earlier in the year, they remain lower than a year ago and are essentially at the long-term historical average. Income gains are also outpacing home price growth by a small margin in most parts of the country.” — Lawrence Yun, NAR’s Chief Economist

Related posts

.png)

Jobs Data Signals a Cooling Labor Market

FAQ: Will paying off my credit cards before applying for a mortgage help?

.png)

Annual Inflation Eases, Fed Leaves Rates Unchanged

Ready to close more deals?

ListReports automatically delivers personalized marketing collateral to your inbox helping you engage with your customers and prospects.