Inflation remains tame, existing home sales edge higher, and Q4 GDP gets revised significantly lower. Here are the key takeaways.

- Annual Core Inflation Hits Nearly Five-Year Low

- Existing Home Sales Edge Higher in February

- Housing Starts Rebound but All in Multi-Family

- At a Glance: GDP, Unemployment and Job Openings

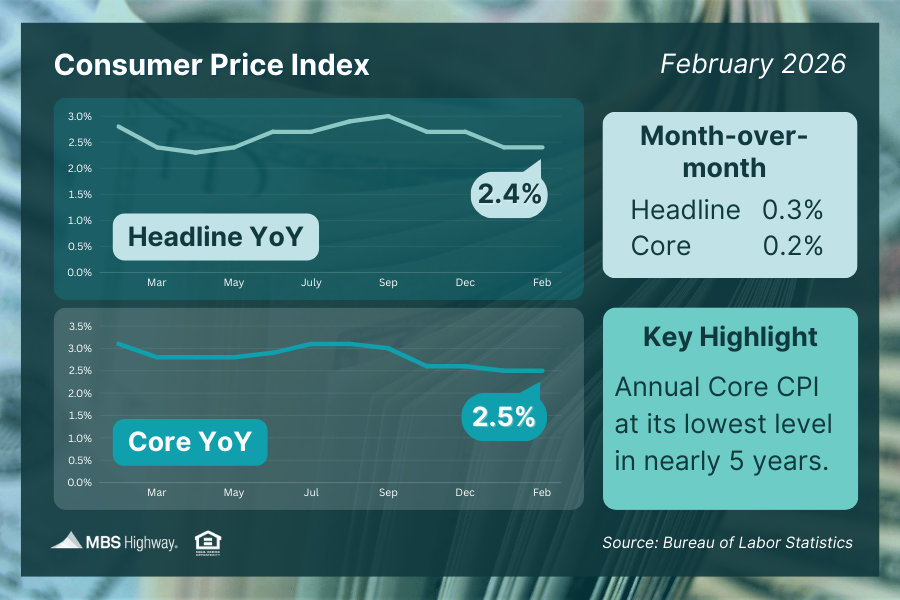

Annual Core Inflation Hits Nearly Five-Year Low

Consumer prices rose 0.3% in February and 2.4% year over year, holding steady from the previous report. Core inflation, which excludes food and energy, increased 0.2% for the month and held at 2.5% annually – its lowest level since March 2021.

Shelter remains a key contributor to inflation, accounting for about 36% of headline CPI and roughly 45% of core CPI. In February, shelter costs were relatively mild, with rent rising just 0.1%, the smallest monthly increase in five years. This helped ease overall inflation pressures.

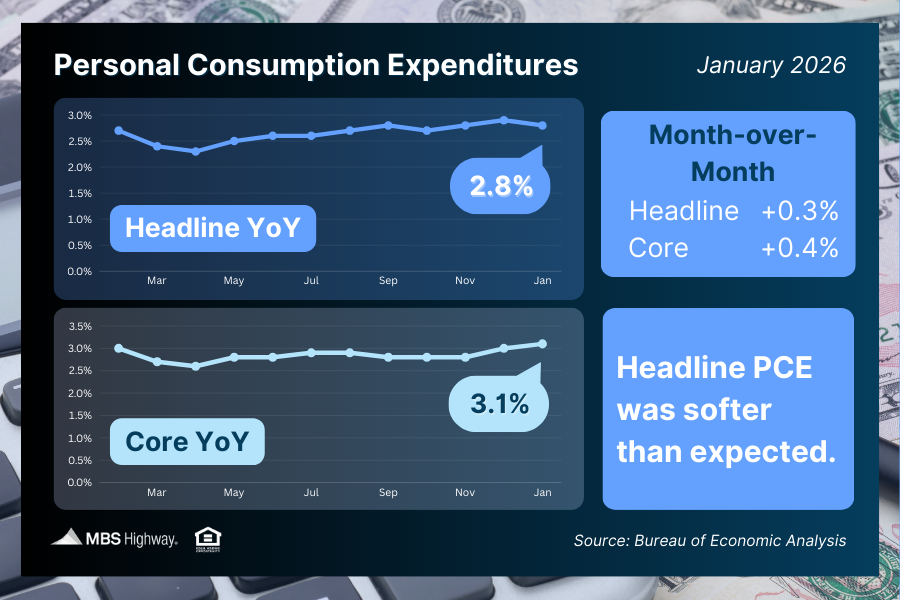

The government also released January’s Personal Consumption Expenditures (PCE) index, the Federal Reserve’s preferred inflation gauge, which had been delayed due to the government shutdown. The report showed headline rose 0.3% for the month, slowing the annual rate to 2.8% from 2.9% while expected to remain at 2.9%. Core inflation, which excludes food and energy, increased 0.4%, bringing the annual core rate to 3.1% from 3%.

What’s the bottom line? The Federal Reserve continues to weigh progress on inflation against signs the labor market is slowing. Sticky inflation supports a cautious approach to rate cuts, while softer employment data could strengthen the case for easing later this year.

The Fed held its benchmark Federal Funds Rate steady in January after three quarter-point cuts late last year. While this rate doesn’t directly determine mortgage rates, it influences borrowing costs across the broader economy.

Fed Chair Jerome Powell has said there is “no risk-free path,” emphasizing that both inflation and labor market trends will guide policy decisions in the months ahead. Geopolitical developments, including the ongoing conflict involving Iran and the recent rise in oil prices, are another factor markets are watching, as higher energy costs can add to inflation pressures.

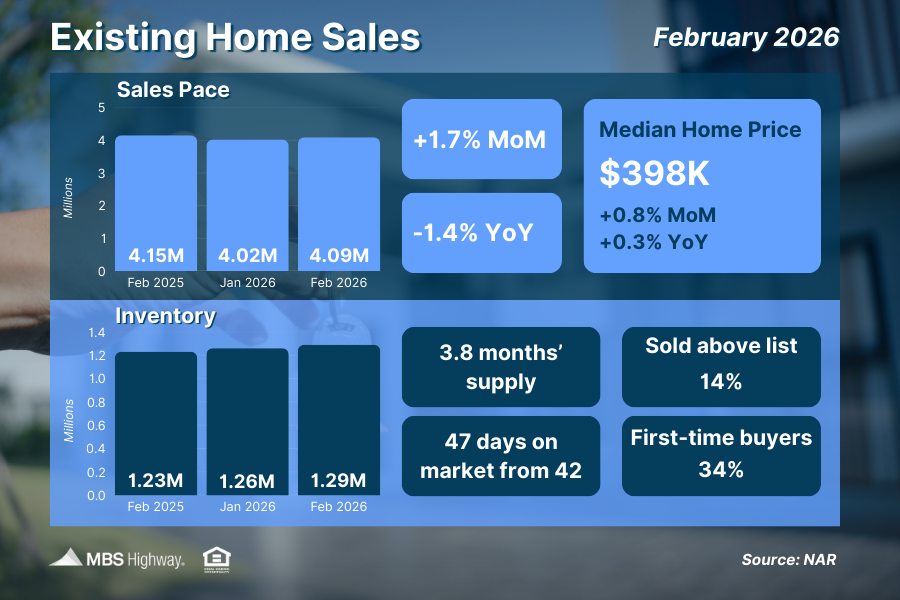

Existing Home Sales Edge Higher in February

After declining in January, existing home closings rose 1.7% in February, according to the National Association of REALTORS® (NAR). Housing inventory also increased, rising 2.4% from January to 1.29 million homes. That’s 4.9% higher than the same time last year.

What’s the bottom line? Housing affordability is gradually improving, which is helping bring some buyers back into the market, according to NAR Chief Economist Lawrence Yun. However, while inventory is growing, it’s doing so slowly. Yun noted that if demand strengthens faster than supply in the coming months, home prices could face renewed upward pressure – underscoring the need for more housing supply.

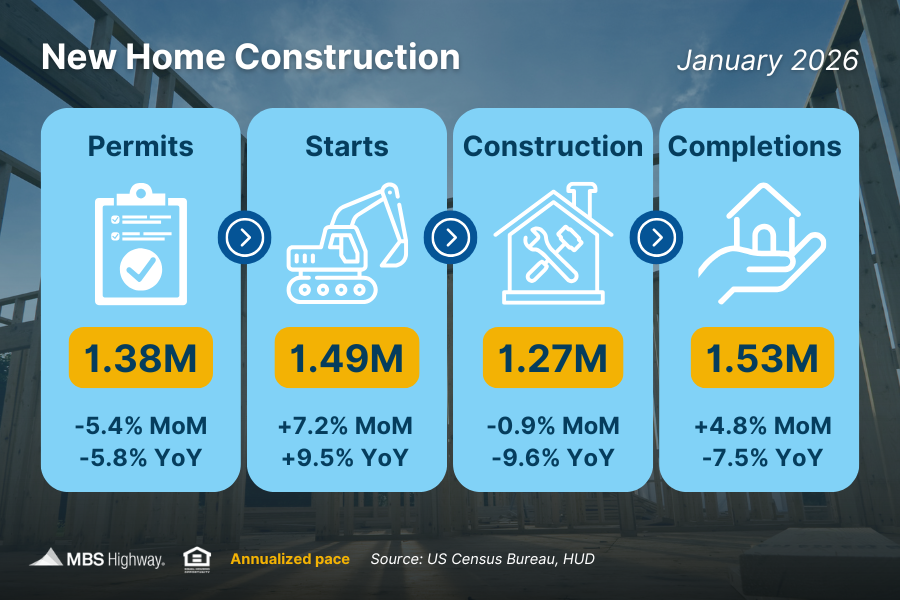

Housing Starts Rebound but All in Multi-Family

Housing starts unexpectedly increased, but the rise was entirely driven by multi-family construction. Multi-family starts had remained subdued ahead of this report, which pointed to potential pressure on rental prices that could contribute to higher inflation. However, with multi-family starts jumping 30% in January alone, that concern would be less significant if this trend continues. Single-family starts, meanwhile, declined.

Housing permits moved lower for both single-family and multi-family units, suggesting that despite the increase in starts, there is less future supply in the pipeline.

What’s the bottom line? The increase in housing starts was driven entirely by a surge in multi-family construction, which could help ease rental inflation if the trend continues. However, declining permits signal weaker future supply, particularly in single-family housing.

At a Glance: GDP, Unemployment and Job Openings

The second estimate of Q4 2025 GDP showed the U.S. economy grew at an annualized rate of 0.7%, down sharply from 4.3% in Q3 and the first Q4 estimate of 1.4%. The drop was driven in large part by cuts in government spending during the shutdown.

Initial jobless claims fell by 1,000 last week to 213,000, while continuing claims fell by 21,000 to 1.850 million. The fact that initial claims have remained low could be pointing to unemployed workers turning to gig work as they are not captured in this data.

Job openings rose to 6.95 million in January from 6.5 million in December, well above market expectations, and remain far below the 2022 peak of more than 12 million. Because some remote roles are posted across multiple states, the true number of available jobs may be even lower.

Related posts

.jpg)

Weekend Talking Points - 'Now Hiring'

FAQ: What does debt-to-income ratio mean?

.png)

Inflation Ticks Higher, Housing Appreciation Forecasts Hold Firm

Ready to close more deals?

ListReports automatically delivers personalized marketing collateral to your inbox helping you engage with your customers and prospects.