.jpg)

ADP’s November jobs data renewed concerns about the labor market (especially small businesses) and the economy as a whole. A rate cut on December 10 now seems likely, and average mortgage rates are approaching 6% again. Transaction volumes are starting to recover.

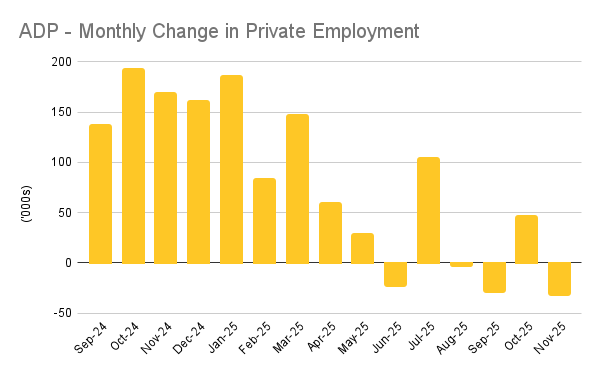

ADP: Big job losses in November. The market was expecting a small positive number (10K-20K in gains). Instead, ADP reported that private employers shed a net 32K jobs in November, with 120,000 lost by small companies alone (medium and large companies added 90K). [More on this later]

TP: This is the last big jobs report that Fed members will receive before their FOMC meeting on December 9–10. Over the last two weeks, the odds of a rate cut have whipsawed from ‘no way’ to ‘without a doubt’.

Challenger: jobs cut remain elevated. Through November, companies have announced 1.17 million job cuts — only the sixth time since 1993 that jobs cuts through November have exceeded 1.1 million. By the way, in three of the other five instances (2001, 2009 and 2020), the US economy was in recession.

October pending home sales were encouraging. NAR’s Pending Home Sales Index rose 1.9% MoM in October. According to my model, that suggests that existing home sales for November could hit 4.2 million (SAAR), which would be the highest figure since February 2025.

TP: The longer mortgage rates stay down near 6%, the more momentum we’re going to get. Add in home price drops in some markets and affordability is improving significantly.

Realtor.com forecasts a boring 2026. I don’t think I can take another year of 4 million existing home sales, but that’s pretty much what Realtor.com’s economics team is forecasting.

- Existing home sales: 4.13 million (+1.7% YoY)

- 30-yr Mortgage rates: 6.3% (average), 6.3% (year-end)

- Median home prices: +2.2% YoY

- Existing homes for sale (inventory): +8.9% YoY

- Rent Growth: -1.0% YoY

TP: In contrast, the National Association of Realtors is forecasting 14% growth in existing home sales with 4% price growth. Granted, the NAR is an industry association, so it tends to keep things optimistic. Ultimately, the key variable is the mortgage rate. If mortgage rates drop below 6%, I think we’re going to have at least 4.5 million existing home sales.

Rental rates keep trending lower. National rents fell 1% month-over-month in November, and are now 5% below their mid-2022 peak. That should be good news for inflation, as “shelter costs” make up a huge percentage of the CPI and PCE price indexes. [Apartment List]

TP: The national multifamily (apartments) vacancy rate remained at 7.2%, a record high for the Apartment List index. While housing permits and starts have slowed, apartment completions continue to run at a high level. With that in mind, it seems unlikely that national rents will move significantly higher in 2026.

ADP data was even worse than it looked.

With its new weekly “NER Pulse” report and consistent monthly data right through the government shutdown, ADP’s private payrolls data has become much more than just a prelude to the Bureau of Labor Statistics report. These days, the market reacts swiftly to the ADP report; and the November ADP data was both disappointing AND concerning.

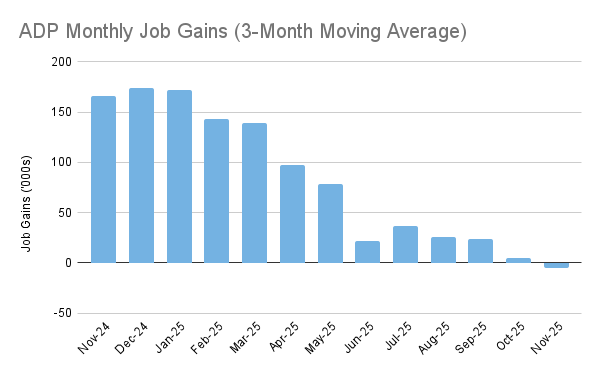

Headline: 32K in net job losses was a lot worse than expected. It’s also the fourth negative number in six months, and the first month that the 3-month moving average has gone negative. You don’t need to be a statistician to discern the clear downtrend.

Sectors: In November, 6 of the 10 sectors tracked by ADP reported job losses, with the largest coming from Professional/Business Services (-26K), IT (-20K), and Manufacturing (-18K). The only sectors still showing decent employment growth? Education/Health Services (+33K) and Leisure/Hospitality (+13K). And Education/Health Services employment seems to grow no matter what the economy is doing (ageing population?).

Company Size: This was the biggest shock from the report. Smaller companies (1–49 employees) shed 120K jobs in November. You might think well, those are just small companies, so who cares? But small companies represent 43% of total private employment! They are the lifeblood of the American economy, a million mom-and-pop businesses, and the nurseries of unicorns.

They’re also the first to feel the pinch from rising costs (raw materials, tariffs, wages?) and the quickest to take action. And that’s exactly what they’re doing, with job losses at both very small and small businesses accelerating. Canaries? Poison gas in the coal mine?

Wages: When the job market was hot, it made a lot of sense to jump ship. In mid-2022, “job changers” were being rewarded with 16% annual wage increases, while “job stayers” were only getting +8%. That’s an 8% wage premium to switch jobs. Today, that switching premium is just 1.9% — hardly worth the effort. This is the “no hire, no fire” job market you’ve been reading about, and it is certainly not indicative of a “strong” labor market.

But will the BLS see things the same way? Probably not. First, because the BLS report includes government jobs, which have likely risen since the shutdown. Second, because the BLS uses its flawed birth/death model to estimate small business employment. ADP’s real data is capturing more ‘births’ than ‘deaths’, while BLS’ birth/death model is slow to capture turning points.

In any case, we won’t get the next BLS data until December 16 — after the final FOMC meeting of the year. That will be for the month of November. And we won’t get October data because of the shutdown.

Bond and Mortgage Market

A few weeks ago, I wrote that “it looks like the Fed is finished for 2025.” What a difference a few weeks make! Since then, we’ve had dovish comments from several senior Fed members, and anemic weekly and monthly jobs growth from ADP. All of a sudden, the market is (once again) convinced that a third rate cut will happen on December 10.

Note: After the rate cut on Oct 29, the Fed Funds Rate policy range is now 3.75–4.00%. The probabilities below come from the CME Group website and are implied from the Fed Funds Rate futures market.

- December 10 FOMC Meeting: 89% probability that rates will be 25 bps below current (was 40% two weeks ago). In other words, the market thinks that there is a very strong chance of a rate cut next week.

- January 28 FOMC Meeting: 65% probability that rates will be 25 bps below current. That implies a 25 bps rate cut at one, but not both, of the December and January meetings. 28% probability that rates will be 50 bps below current, which implies a rate cut at both the December and January meetings.

They Said It

“Hiring has been choppy of late as employers weather cautious consumers and an uncertain macroeconomic environment. And while November’s slowdown was broad-based, it was led by a pullback among small businesses.” — Nela Richardson, ADP’s Chief Economist

Related posts

Home Sales Rise While Economic Growth Slows

Weekend Talking Points – ‘Spike’

March 2026 MBS Highway Housing Index

Ready to close more deals?

ListReports automatically delivers personalized marketing collateral to your inbox helping you engage with your customers and prospects.