.jpg)

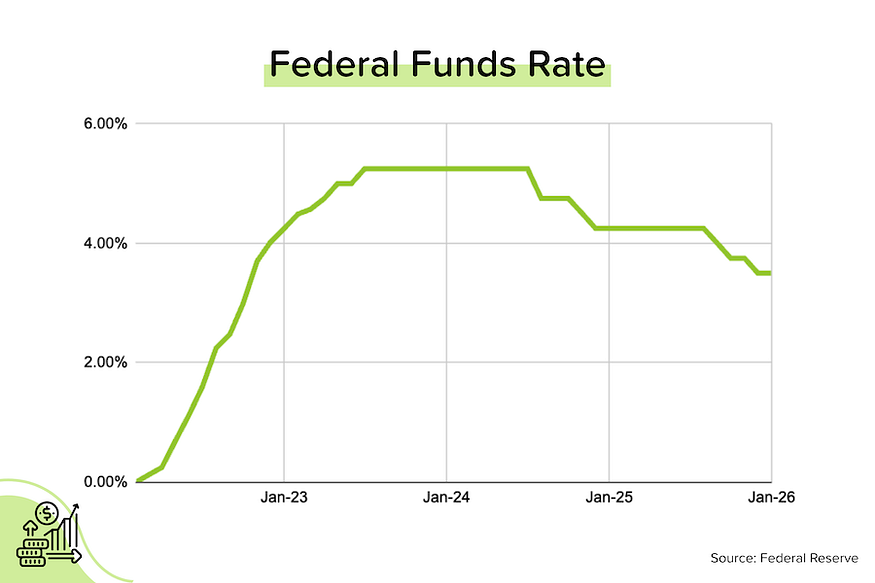

The Fed kept rates steady at their latest meeting, citing stubbornly high inflation and low unemployment. And Jerome Powell implied that rates might be on hold for a while. A new Fed Chairman should be announced soon (but he won’t assume the role until May). Meanwhile, more signs of improving buyer demand in the Case-Shiller home price numbers.

Very strong GDP growth. The US economy grew at an annualized pace of 4.4% in the 3rd quarter of 2025, even stronger than the +3.8% annual pace reported for the 2nd quarter of 2025. These are very large numbers for an economy as huge and developed as the United States. As usual, the majority of the growth came from Private Consumption (you and me buying stuff). The problem is that already-indebted American consumers continue to buy on credit — the savings rate was just 3.5% in November 2025, having consistently fallen from ~5% earlier in the year.

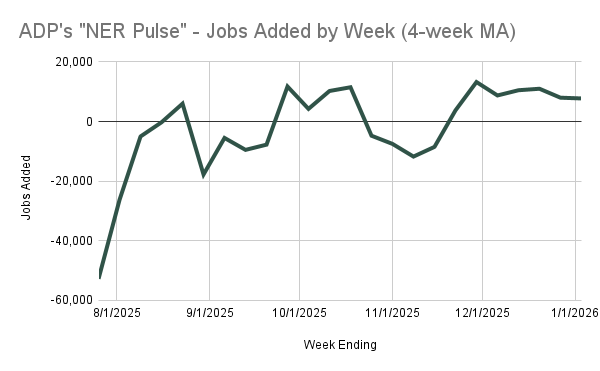

But nearly jobless GDP growth. ADP reported that private employers added an average of 7,500 jobs per week over the last month. That’s a pace of roughly 30K per month, which is almost nothing for a country our size. Great GDP, but almost no jobs growth? This is either a productivity miracle or there’s something else happening. [ADP]

Case-Shiller indexes see trend reversal. For most of 2025, growth in Case-Shiller’s national home price index has been slowing: from +4.2% year-over-year in January 2025 to 1.3% YoY in September 2025. But we’ve seen a reversal lately, with prices rising by 0.4% month-over-month in both October and November 2025. As we’re seeing elsewhere, lower mortgage rates are starting to boost buyer demand AND prices. [S&P Cotality]

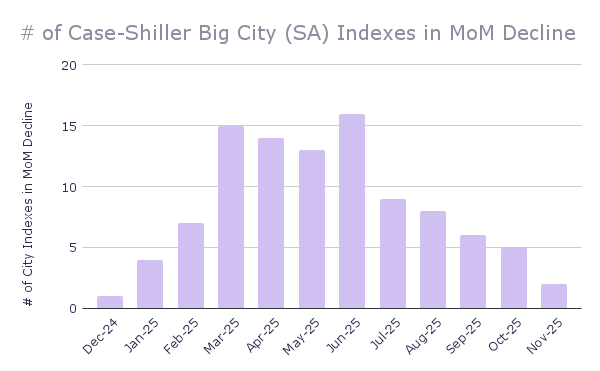

TP: At the national level, prices are flattish. But price momentum is shifting upwards, and it’s pretty broad-based. In June 2025, 16 of the 20 Big City home price indexes fell on a month-over-month basis. By August 2025, only 8 Big City indexes fell MoM. And in November 2025, only 2. If you annualize the last three months of MoM data (0.23% + 0.42% + 0.40%) X 4, you get +4.2% YoY.

Fed kept rates steady. This was really no surprise. In fact, the market isn’t fully pricing-in a rate cut until the June 17 FOMC meeting. Powell’s official statement was mostly boiler-plate: inflation is still too high, and the unemployment rate remains very low. But what was a little surprising was Powell’s intimation that rates could be on hold for many months.

TP: Powell’s replacement as Federal Reserve Chairman should be announced soon by the Trump Administration. Whoever it is will certainly be more dovish (inclined to cut rates) than Powell, but the new guy will still only have one vote. How skilled and successful he will be at building consensus for additional rate cuts is uncertain.

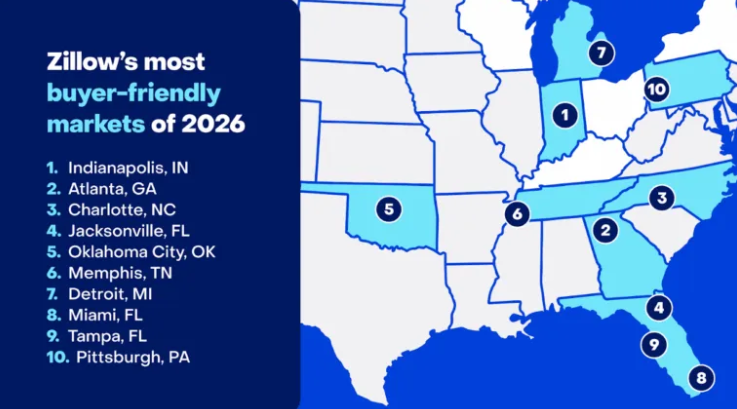

Zillow’s “best markets for homebuyers” 2026. Zillow looked for cities: 1) where prices have been trending down lately, but 2) the long-term outlook is strong, and 3) affordability is (relatively) good. Indianapolis was ranked #1, followed by Charlotte, in what was a very Midwestern and Southern city-heavy list.

TP: We’ve been writing a lot about where prices have been falling, focusing on places like Austin, Tampa, and Nashville. The key thing to remember is that affordability has improved a lot in these cities (lower prices + lower rates), and new people are still moving in. If you’re a property investor, it’s a good time to be looking at some of these markets.

On the Case (Shiller) Again for November 2025

Annual price growth for Case-Shiller’s seasonally-adjusted national index was flat at +1.4% YoY in November 2025. (We started the year at +4.2% YoY!) That doesn’t seem very exciting until you look under the hood: 1) price growth has been 0.4% month-over-month for the last two months, and 2) the majority of Big City indexes are now growing MoM. Why? Lower rates.

As we do each month, we looked at the 20 Big City indexes in detail. Here’s what we found:

- Only 2 of the 20 big city indexes saw their SA indexes decline MoM in November 2025 (way down from 16 in June 2025). And those price drops were modest: Boston (-0.15% MoM) and Cleveland (-0.10% MoM).

- The largest increases came from San Diego (+1.20% MoM), Phoenix (+0.99%), Las Vegas (+0.85% MoM) and Los Angeles (+0.77%). All four of these cities were seeing prices drop MoM for most of 2025, so these are important recoveries to watch.

- Only 6 of the 20 big cities are still seeing YoY price declines in their SA indexes (down from 9 last month): Tampa (-3.8% YoY), Dallas (-1.4% YoY), Denver (-1.3% YoY), Miami (-1.0% YoY), Las Vegas (-0.4% YoY) and Seattle (-0.1%).

- Four cities made new all-time highs in November 2025: Chicago, Detroit, Minneapolis, and New York City.

- Six cities’ price indexes are still below their mid-2022 peak levels: San Francisco (-5.6%), Phoenix (-3.6%), Denver (-3.0%), Dallas (-2.4%), Portland (-2.0%), and Seattle (-1.5%).

Reminder: The Case-Shiller index is the gold standard for measuring home price growth because it uses the repeat sales method (looking at ‘pairs’ of transactions for the same home) to more accurately gauge true appreciation. However, this accuracy comes at a cost: a nearly two-month time lag.

Bond and Mortgage Market

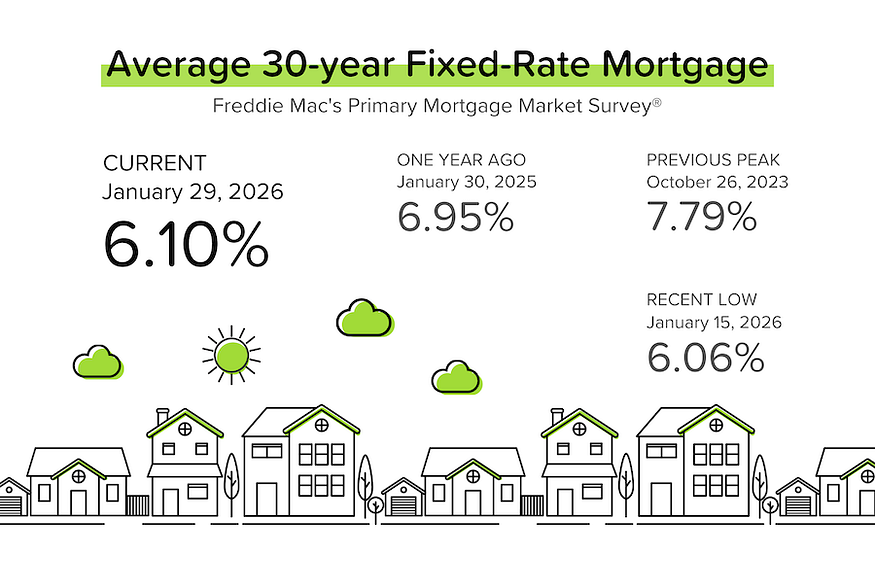

The Fed did nothing, which was expected. Powell’s language was perhaps a bit more hawkish than expected, but not dramatically so. President Trump didn’t reveal his pick for the next Fed Chairman. So mortgage rates haven’t really done much this week, and remain near 6.10%, according to the latest lender survey from Freddie Mac.

Note: The Fed Funds Rate policy range is currently 3.50–3.75%. The probabilities below come from the CME Group website and are implied from the Fed Funds Rate futures market.

- March 18 FOMC Meeting: 87% probability that the Fed Funds Rate target range is kept at 3.50–3.75% (was 78% a week ago). In other words, no rate cut at the March FOMC meetings. Only a 13% probability that rates are 25 bps below current (was 22% last week), which would imply a 25 bps rate cut at the March meeting.

- April 29 FOMC Meeting: 71% probability that the Fed Funds Rate target range is kept at 3.50–3.75%. In other words, no rate cut at EITHER the March or April meeting. 27% probability that rates will be 25% below current, which implies a 25 bps rate at either the March (unlikely) or April (more likely) meeting.

They Said It

“After the three recent rate cuts, we’re well-positioned to address the risks that we face on both sides of our dual mandate. [We] haven’t made any decisions about future meetings, but the economy is growing at a solid pace. The unemployment rate has been broadly stable, and inflation remains somewhat elevated. So we’ll be looking at our goal variables and letting the data light the way for us.” — Jerome Powell, Federal Reserve Chairman

Related posts

FAQ: What home price is right for me?

.png)

Home Sales Slip, Wholesale Inflation Cooler Than Expected

Weekend Talking Points – ‘Not Over Yet’

Ready to close more deals?

ListReports automatically delivers personalized marketing collateral to your inbox helping you engage with your customers and prospects.