.jpg)

With mortgage rates remaining in the low 6% range for several months now, transaction activity is clearly picking up. Is 2026 going to be the recovery year that we’ve been waiting for? And while the market is skeptical that the Fed will cut rates again on January 28, the latest data from ADP and the JOLTS report evidences an economy that is struggling to create much job growth.

Encouraging November pending sales. Lower rates are (finally) boosting transaction volumes! The National Association of Realtors’ Pending Home Sales Index (PHSI) rose 3.3% month-over-month to 79.2. That’s the highest index level seen since February 2023. It implies that December existing home sales should come in between 4.3–4.4 million units SAAR (seasonally-adjusted, annualized rate).

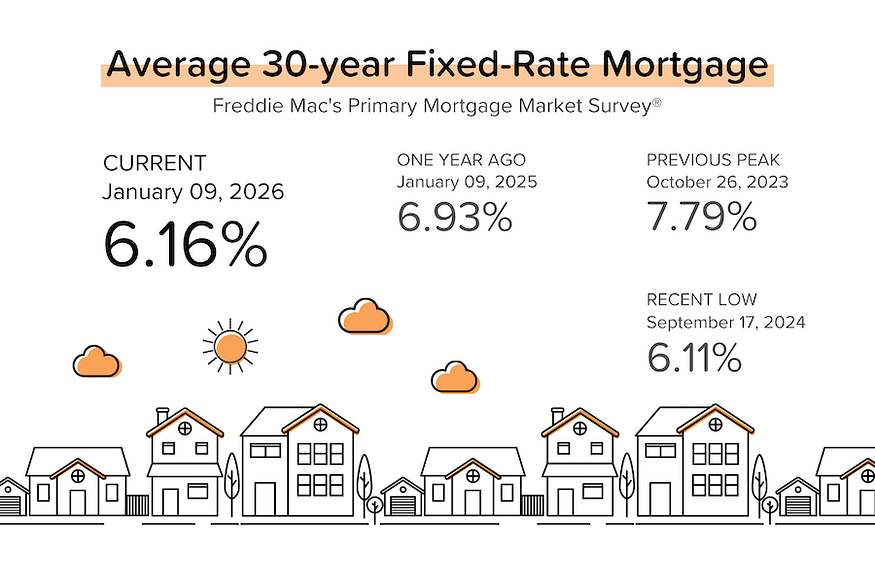

TP: Lower mortgage rates are great, but it’s better when rates remain lower for longer. With average 30-year mortgage rates staying below 6.50% since early September, and hovering around 6.25% since late November, transaction activity is finally starting to pick up.

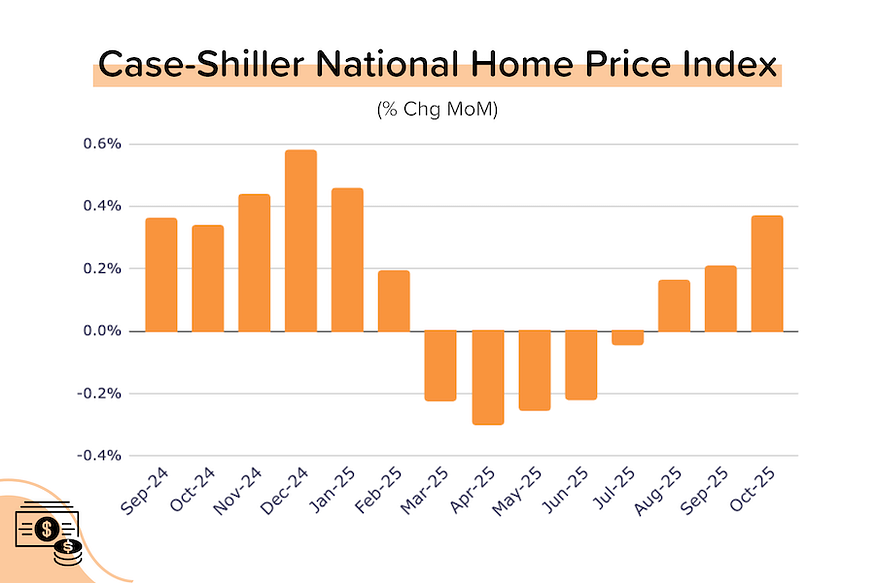

Case-Shiller index shows price growth starting to perk up. In October 2025, Case-Shiller’s national seasonally-adjusted home price index climbed 0.4% MoM, following a 0.2% MoM rise in both August and September. On a year-over-year basis, price growth remained low (+1.4% YoY), but did accelerate from +1.3% YoY in September.

TP: When price growth is flattish nationwide, that means that some markets are up, while others are down. In fact, half of Case-Shiller’s 20 “big city” indexes are down YoY, with the biggest declines in Tampa (-4.2% YoY) and Phoenix (-1.5%). On the other side, the Midwest and Northeast continue to see solid price growth: Chicago (+5.8% YoY), New York (+5.0% YoY), and Cleveland (+4.1% YoY).

A big drop in job openings. The JOLTs report for November showed that job openings dropped to 7.15 million — which was a lot lower than expectations. Apart from September 2024 (when job openings briefly dipped to 7.10 million), that’s the lowest figure we’ve seen since late 2020! [BLS]

Slow job growth continues. According to ADP, private employers added 41,000 jobs in December 2025. While that was a turnaround from -29,000 in November, it’s still very low. Over the last 6 months, the average monthly job gain was just 22,000. [ADP]

TP: This is not the kind of monthly job growth you’d expect from an economy that grew at 4.3% annualized in 3Q 2025! All eyes will be on the BLS jobs report this Friday, where the market is expecting 60,000–70,000 in job gains, with the unemployment rate dropping to 4.5% (after surging to 4.6% in part due to the government shutdown).

Trump wants to keep big investors out of the SFH market. As with most of President Trump’s initial pronouncements, the plan was short on details. But his goal was clear: stop giant landlords like Invitation Homes from competing with real humans trying to buy their first home. There are several problems with this, however. First, big investors like Invitation Homes and Cerberus only own 2–3% of single-family homes nationwide — so the impact would be limited in most markets. Second, how do you define a ‘large’ property investor? More than 1,000? More than 10?

TP: Personally, I think this is a great idea. The increasing commoditization of the SFH market is bad for society. But as tempting as it is to scapegoat Blackrock and Invitation Homes, institutional investors weren’t the primary reason for the affordability crisis we have today. It would be more accurate to place the blame with local zoning regulations, COVID, the Fed, and small-scale (but large in aggregate) property investors like me.

Bond and Mortgage Market

Over the last few weeks, average 30-year mortgage rates moved below 6.25% and stayed there. The most recent jobs data (ADP, JOLTs) has been quite weak, but the BLS jobs report out Friday, January 9 is always a wild-card. In addition, the bond market was rattled lately by Trump’s desire to massively boost military spending in 2027. A lot more debt on the way?

Note: After the rate cut on Dec 10, the Fed Funds Rate policy range is now 3.50–3.75%. The probabilities below come from the CME Group website and are implied from the Fed Funds Rate futures market.

- January 28 FOMC Meeting: 88% probability that the Fed does nothing; only a 12% probability of a 25 bps rate cut.

- March 18 FOMC Meeting: 41% probability that rates are 25 bps below current. That means a rate cut at either the January 28 (unlikely) or the March 18 (more likely) meeting, but not at both. 59% probability that the Fed Funds Rate target range is kept at 3.50–3.75%. In other words, no cut at either the January or March FOMC meetings.

They Said It

“For a very long time, buying and owning a home was considered the pinnacle of the American Dream. It was the reward for working hard, and doing the right thing, but…that American Dream is increasingly out of reach for far too many people, especially younger Americans. It is for that reason, and much more, that I am immediately taking steps to ban large institutional investors from buying more single-family homes, and I will be calling on Congress to codify it. People live in homes, not corporations.” — President Donald J. Trump

“Homebuyer momentum is building. The [pending home sales] data shows the strongest performance of the year after accounting for seasonal factors, and the best performance in nearly three years, dating back to February 2023. Improving housing affordability–driven by lower mortgage rates and wage growth rising faster than home prices–is helping buyers test the market. More inventory choices compared to last year are also attracting more buyers to the market.” — Lawrence Yun, NAR’s Chief Economist

Related posts

.png)

Jobs Data Paints a Mixed Picture

.jpg)

Weekend Talking Points - 'No Hike, No Cut'

.png)

The Wealth Building Power of Homeownership

Ready to close more deals?

ListReports automatically delivers personalized marketing collateral to your inbox helping you engage with your customers and prospects.