.jpg)

Oh my! That April CPI! Inflation surged on higher energy prices, which affect a lot more than just gasoline and jet fuel prices (airline tickets, fertilizer, etc.) So far, the housing market is showing resilience, but there is little doubt that higher mortgage rates are keeping spring/summer transaction volumes more muted than they would be otherwise.

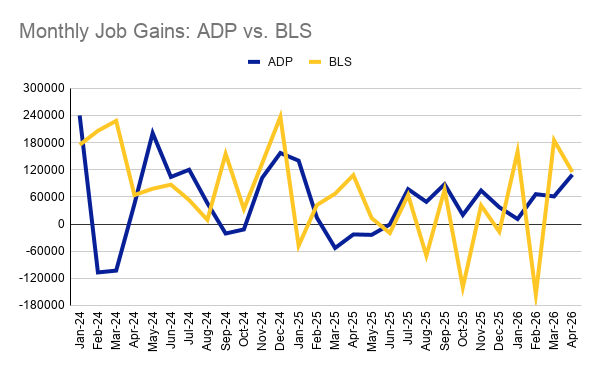

BLS: Economy added 115K jobs in April. While better than expected, April’s job growth was still modest. Over the last 12 months, only 251K net new jobs were created. The unemployment rate was steady at 4.3%. Meanwhile, the negative revisions continue: February’s original -92K number ended up at -156K after two revisions. [BLS]

TP: Just look at the volatility of the BLS’ monthly jobs numbers! It looks like a Bitcoin price graph! Meanwhile, ADP’s monthly data has shown a clear — and fairly smooth — acceleration in job growth in 2026.

Still stuck at 4 million. April existing home sales rose 0.2% month-over-month to 4,020,000 units sold (on a seasonally-adjusted, annualized basis). For 3+ years, existing home sales have been stuck in a very narrow range between 3.9 million and 4.2 million units sold (SAAR). That pace of sales is comparable to 1995 (when the USA had 70 million fewer people) and 2008–2011 (after the housing bubble burst). The reasons for the subdued sales today are well-known, but are worth repeating:

- Affordability Crisis — National home prices rose 47% between 2019–2023 and average mortgage rates climbed from 3% to a high of 8% between 2021–2023 (as the Fed raised rates by 525 basis points = 5.25%). This was a brutal combination for would-be buyers.

- I Ain’t Moving — People who purchased homes (or refinanced) during 2020–2021 enjoyed exceptionally low mortgage rates. They are naturally loath to give those rates up, even if they would prefer to move. There’s also sticker shock: the price for that larger home in that nicer area went up (at least) as much as the price of their current home did.

So both demand and supply got hit. When that happens, transaction volumes fall.

TP: The good news is that affordability has been improving lately (lower mortgage rates AND lower home prices in many markets). Plus, the ‘lock-in’ effect is fading with time: eventually the psychological need to move (twins on the way!) overcomes the financial concern (don’t want to give up my 3% rate).

April CPI, oh my! We knew it was coming, and it finally arrived. Headline CPI (Consumer Price Index = inflation for you and me) jumped to +3.8% year-over-year in April from +3.3% YoY in March. And “Core” CPI (which excludes food & fuel prices) rose to +2.8% in April from +2.6% YoY in March. The main driver was higher energy prices (thanks to the US/Iran conflict), but shelter (housing) costs also jumped due to an accounting anomaly that should disappear next month.

TP: After the scorching April CPI (and PPI) reports, the likelihood of a Fed rate cut during the remainder of 2026 dropped to zero. In fact, the market is now putting a 30% probability on rates being 25 basis points HIGHER than they are today by year-end.

Kevin Warsh confirmed as new Fed Chair by Senate. His confirmation hearings were contentious, focusing on: 1) his and the Fed’s independence given that he is President Trump’s appointee, and 2) his considerable individual and family wealth. Few questioned his qualifications.

TP: Mr. Warsh inherits a deeply divided Fed. He will remain under considerable pressure from President Trump to cut rates, but inflation is resurgent and the job market is (at least superficially) strong. While the Fed Chair’s voice can be highly persuasive in crafting a consensus view, he’s only got one vote.

MBS Housing Survey results for May. After April’s setback, the MBS Highway National Housing Index bounced back in May, gaining 5 points month over month to reach 47. The index now sits 5 points above its level from a year ago, suggesting the underlying trend remains constructive despite month-to-month volatility.

TP: As a reminder, a reading of 50 separates contraction (below 50) from expansion (above 50).

Bond and Mortgage Market

According to Freddie Mac’s weekly PMMS survey, average mortgage rates were roughly flat week-over-week. But given the bond market’s reaction to the scary April CPI figures, market mortgage rates are already moving higher. The market is still pricing in ZERO Fed rate cuts for the remainder of 2026. In fact, the market is beginning to price in some probability of rate HIKES towards the end of the year.

Note: The Fed Funds Rate policy range is currently 3.50–3.75%. The probabilities below come from the CME Group website and are implied from the Fed Funds Rate futures market.

- June 17 FOMC Meeting: This will be Kevin Warsh’s first meeting as the new Fed Chairman. 99% probability that the Fed Funds Rate will be kept at 3.50–3.75% (was 94% last week).

- July 29 FOMC Meeting: 99% probability that the Fed Funds Rate will be kept at 3.50–3.75% (was 88% last week).

- September 16 FOMC Meeting. 88% probability that the Fed Funds Rate will be kept at 3.50–3.75%. An 11% probability that rates will be 25 basis point HIGHER than they are today.

- No rate cuts in 2026? If I look way out to the last FOMC meeting of the year (Dec 9), the market is pricing in a 62% probability (was 72% last week) that the Fed Funds Rate will be exactly where it is today. Additionally, the market is now pricing in a 37% probability that rates will be at least 25 basis points (and maybe 50 basis points) higher by year-end.

They Said It

“Despite mixed macroeconomic signals — including a record-high stock market and historically low consumer confidence — home sales were modestly boosted by the continued improvement in housing affordability. Mortgage rates are lower from a year ago, and average income growth is outpacing home price gains.

Inventory still remains tight. Multiple offers, though not as intense as a few years ago, are still occurring. At the same time, days on market are lengthening on average, implying that consumers are taking their time before making decisions.” — Lawrence Yun, NAR’s Chief Economist

Related posts

.png)

Annual Inflation Eases, Fed Leaves Rates Unchanged

FAQ: Can I make a big purchase before closing on my home?

.png)

Home Sales Rebound, Oil Markets Stay Volatile

Ready to close more deals?

ListReports automatically delivers personalized marketing collateral to your inbox helping you engage with your customers and prospects.