.jpg)

The data vacuum continues. We didn’t get retail sales this week, but we will get CPI next week. Meanwhile, commentary from Jerome Powell and other Fed members helped 10-year treasury yields drop below 4% and 30-year mortgage rates approach 6%.

Powell says QT could stop soon. Quantitative tightening (the Fed selling assets) is the reverse of quantitative easing (the Fed buying assets). QE was about bidding up bond prices to keep yields/interest rates lower to support the economy. QT has been about unwinding that stimulus, and that exerts a downward influence on bond prices and keeps yields higher than they might be otherwise. QT has been happening since 2022. Powell suggested it could end in the next few months. He also had the following to say about QE:

“With the clarity of hindsight, we could have — and perhaps should have — stopped asset purchases sooner.” — Jerome Powell, Federal Reserve Chairman

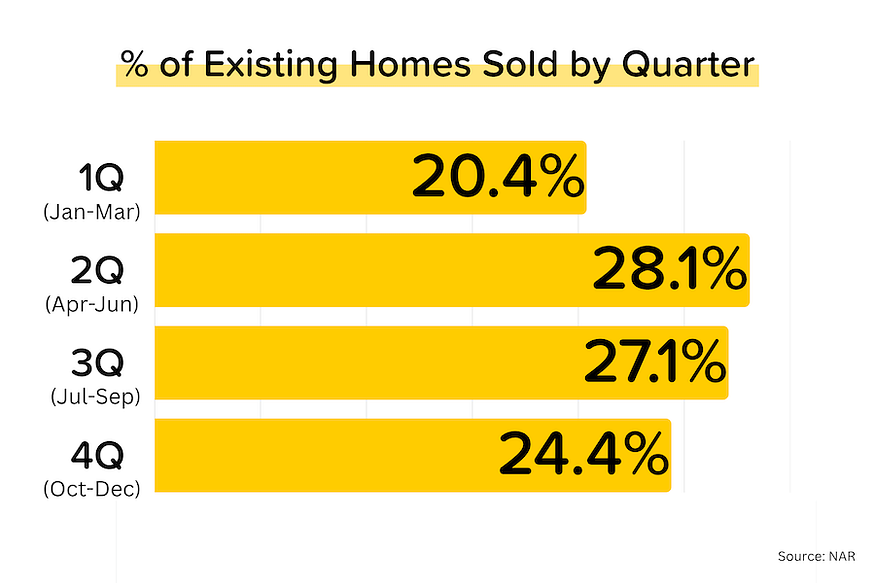

’Tis the seasonality. You know that real estate is a seasonal business, but do you know how seasonal? If transaction volumes were spread equally across the year, you’d expect 25% of sales to happen each quarter. What actually happens is that spring (2Q = April-June) is the strongest month (28% of annual sales), followed closely by summer (3Q =July-September). Things start to slow down in the fall/early winter (4Q = Oct-Dec), but it’s the first quarter (1Q = January-March) that is the slowest by far.

TP: There are well-known reasons for this seasonality. One is the weather (especially in the northern states), and the other is school (parents don’t want to move their kids to a new school district mid-year). As you’d expect, the seasonality is much more pronounced in states like Alaska, North Dakota and Michigan. And inventory levels fall as the low season approaches (why keep a home listed that isn’t likely to sell). That said, the fall/early winter period can offer flexible buyers a nice combination of decent inventory levels and far less competition.

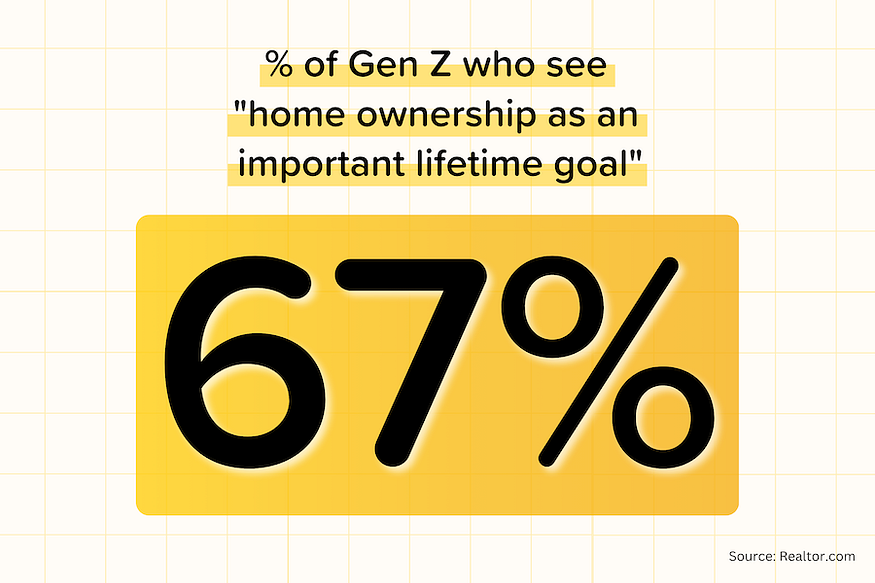

Gen Z still wants a home. According to a survey commissioned by Realtor.com, 67% of Gen Z adults (aged 18–27) see homeownership as “an important lifetime goal”, and 69% said that real estate was “an opportunity to generate wealth.” Sensibly, they’re much more focused on building their careers first so that they can save for a down payment later. Despite affordability issues, the kids are all right. [Realtor.com]

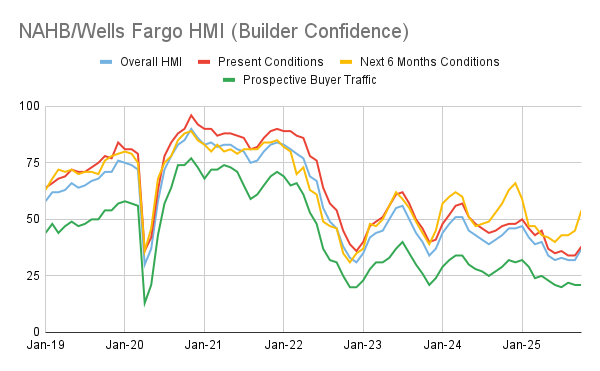

Builder confidence boosted. The National Association of Homebuilder’s confidence index jumped from 32 → 37 in October (highest since April 2025) and its forward-looking sub-index (outlook for the next 6 months) rocketed from 45 → 54. [NAHB]

TP: As a reminder, for this survey >50 = bullish and <50 = bearish. So overall, builders are still bearish (37), but they’re getting a lot more bulled-up about the future (54). Why? Simple: mortgage rates trending lower, and the potential for further Fed rate cuts before year-end.

Rents continue to see modest YoY declines. In September, national asking rents declined YoY for the 26th straight month. That’s a long time. But they’re still only 3.2% below their August 2022 peak, so the downtrend has been glacial. Where are rental rates down the most? Austin TX (-7.2% YoY), Denver CO (-6.5% YoY), Phoenix AZ (-6.4% YoY), Jacksonville FL (-5.5% YoY) and Cleveland OH (-5.5% YoY). [Realtor.com]

Bond and Mortgage Market

As I write this note, the yield on the 10-year US Treasury has moved below 4%. If we apply the historically typical spread of 1.5%-2.0% (between 30-year mortgage rates and the 10Y UST), we’d get a 30-yr mortgage rate estimate of 5.5%-6.0%. We’re at 6.27% today. I have zero doubt that mortgage rates in the 5% range would bring life roaring back into the housing market — which has been stuck at 4 million unit sales pace for nearly 3 years.

Note: The Fed Funds Rate policy range is now 4.00–4.25%. These probabilities come from CME Group website and are implied from the Fed Funds Rate futures market.

- October 29 FOMC Meeting: 99% probability that rates will be 25 bps below current (was 95% last week). In other words, a second 25 bps rate cut on October 29.

- December 10 FOMC Meeting: 97% probability that rates will be at least 50 bps below current (was 82% last week). 57% probability that rate will be 75 bps below current — in other words, a 25 bps cut on October 29 and a 50 bps cut on December 10. A jumbo rate cut in December? Now that’s new!

They Said It

“The [rise in builder confidence] in October is a positive signal for 2026 as our forecast is for single-family housing starts to gain ground next year. The 30-year fixed-rate mortgage fell from just above 6.5% at the start of September to 6.3% in early October. Combined with anticipated further easing by the Fed, builders expect a slightly improving sales environment, albeit one in which persistent supply-side cost factors remain a challenge.” — Robert Dietz, NAHB’s Chief Economist

Related posts

January 2026 MBS Highway Housing Index

.png)

Soft Jobs Data, Slower Home Construction

.jpg)

Weekend Talking Points - 'Is 2026 the Year?'

Ready to close more deals?

ListReports automatically delivers personalized marketing collateral to your inbox helping you engage with your customers and prospects.