.jpg)

Average mortgage rates are at their lowest levels in more than a year, which is already boosting refi activity and starting to bring buyers off the sidelines. Wouldn’t it be a treat if the September CPI report showed lower than expected inflation?

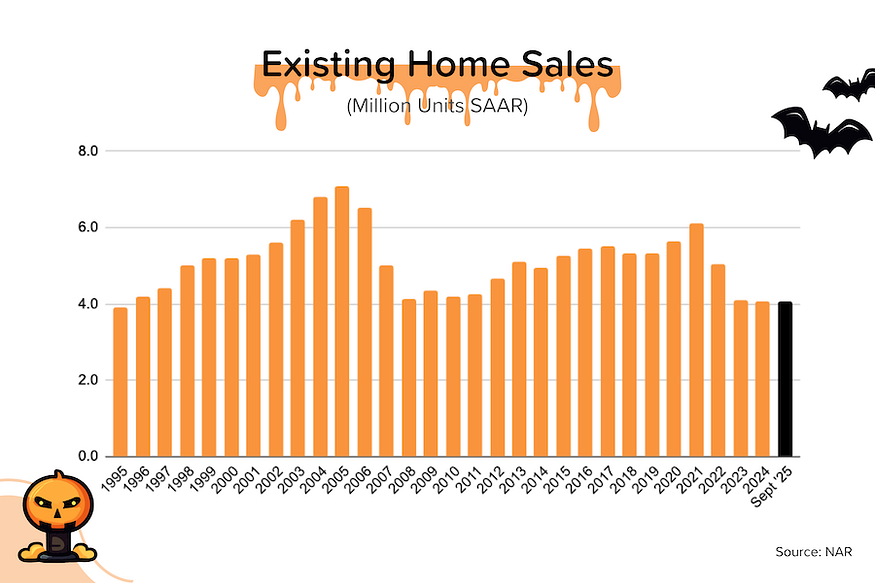

Existing home sales inch higher. September existing home sales rose 1.5% month-over-month to 4.06 million units (SAAR). That might not sound like much — especially considering recent downward moves in mortgage rates — but I actually think it’s quite encouraging. Year-over-year growth was +4.1%. And the “raw” data (the actual sales figure for the month) was up 8.2% YoY.

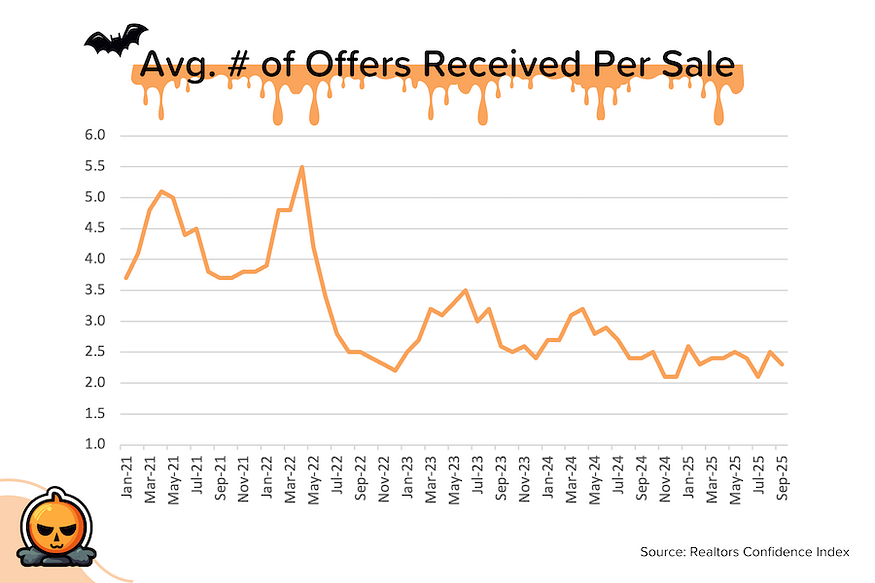

Competition cools. The Realtors Confidence Index for September evidenced the normal seasonal slowdown in competition levels: longer days on market (31 → 33) and fewer competing bids (2.5 → 2.3). That said, taking seasonality into account, competition levels are still cooler than last year.

TP: The combination of lower mortgage rates and (in many markets) lower prices IS bringing buyers off the sidelines. It just takes time. Unlike refis — which can be executed quickly with proper preparation — the home search process takes time: at least 2 months from “We should think about moving” to “I love our new home!”

Twice as many sellers as buyers. I’ve got some issues with the way Redfin estimates the buyer count, but directionally the analysis is on target. In 7 of the Top 50 metros ranked by household size, the number of sellers is at least twice as large as the number of buyers. In Austin, it’s 2.3x. Three of these ‘super buyer’s markets’ were in Florida (Fort Lauderdale, West Palm Beach, and Miami), three were in Texas (Austin, San Antonio, and Dallas) and one was in Tennessee (Nashville). [Redfin]

September CPI (inflation) preview. The market is looking for “headline” CPI to rise from +2.9% YoY → +3.0% YoY, with “core” CPI steady at +3.1% YoY. But our parent company MBS Highway thinks that there is room for a downside surprise given the deceleration in “shelter” costs (44% weighting in “headline” CPI). If so, that would be excellent news for the bond market.

TP: Inflation has been trending higher in recent months, complicating the Fed’s interest rate decisions. Despite this, the market believes that a rate cut at the FOMC meeting next week is a sure thing (because of the weakening jobs data).

The Fault in our SAARs?

The media loves writing stories like “the fall in mortgage rates has failed to bring buyers off the sidelines.” And, to be fair, the 4.06 million units (SAAR) figure we just got for September 2025 existing home sales seems to support those clickbait headlines. After all, we’ve been selling homes at a 4 million unit annual pace for most of the last three years.

But what if I told you that the non-seasonally-adjusted (NSA, or “raw”) figure for existing home sales was up 8.2% year-over-year in September?!

As a reminder, the “raw” data is the actual monthly sales figure. The market actually sold 357,000 existing homes in September 2025. To turn that into a seasonally-adjusted, annualized rate (SAAR), you apply an adjustment factor (to account for seasonality) and then multiply that by 12 (months of the year).

Typically, September (NSA) existing home sales fall by 10–15% month-over-month. It’s a seasonal thing. Happens every year. But in September 2025, they only fell 5.1% MoM. In other words, they fell by much less than normal seasonality would predict.

If not for an adjustment in the seasonal adjustment factor (SAF) used to calculate the seasonally-adjusted pace, the SAAR rate for existing home sales in September could have easily been 4.2 million.

So, we’re actually seeing more of a mortgage rate fall-driven increase in activity than is apparent in the SAAR figures.

2024:

Sept NSA Sales: 330K

SAF: 0.98

Sept SAAR: (330K X 0.98 X 12) = 3.9m

2025:

Sept NSA Sales: 357K (+8.2% YoY as above)

SAF: 0.95

Sept SAAR: (357K X 0.95 X 12) = 4.07m

You might think “0.95 vs. 0.98, who cares?” but if you instead use 0.98 for the Sept 2025 figure, you get 4.2 million SAAR — which would have been up 8% YoY and beat Wall Street estimates.

Moreover, as we move in October and especially November, the SAFs start to really boost the SAAR figure. So if we get an increase in the NSA figures in those months (or at least less of a seasonal fall), we could get a 4.3 or 4.4 million SAAR print EASY.

Bond and Mortgage Market

The yield on the 10-year US Treasury Bond has managed to stay below 4% (at one point last week it was 3.95%) and average mortgage rates (according to Freddie Mac’s weekly survey) have dropped to 6.19% — the lowest rate in over a year. Remember: at the beginning of 2025, average rates were over 7%!

There is a wide range of opinion on where mortgage rates go from here. Barry Habib, the CEO & Founder of our parent company, MBS Highway, thinks that mortgage rates will continue to trend down as the Fed cuts rates, and could go as low as 5.5%. But the majority of forecasters believe rates will stay between 6–7% for the remainder of this year and on into 2026.

Note: The Fed Funds Rate policy range is now 4.00–4.25%. These probabilities come from CME Group website and are implied from the Fed Funds Rate futures market.

- October 29 FOMC Meeting: 99% probability that rates will be 25 bps below current (same as last week). In other words, a second 25 bps rate cut on October 29.

- December 10 FOMC Meeting: 92% probability that rates will be 50 bps below current (was 97% last week). In other words, a third 25 bps rate cut on December 10.

They Said It

“As anticipated, falling mortgage rates are lifting home sales. Improving housing affordability is also contributing to the increase in sales.” — Lawrence Yun, NAR’s Chief Economist

Related posts

January 2026 MBS Highway Housing Index

.png)

Soft Jobs Data, Slower Home Construction

.jpg)

Weekend Talking Points - 'Is 2026 the Year?'

Ready to close more deals?

ListReports automatically delivers personalized marketing collateral to your inbox helping you engage with your customers and prospects.